US Income Tax Calculator Explained for Individuals

Use a US income tax calculator to estimate your federal tax bill, refund, and planning opportunities. Learn how tax brackets, deductions, and credits work in 2026.

Disclaimer: This article provides educational financial information only and does not constitute tax or financial advice. Always consult a qualified tax professional before making any tax planning decisions. Results from any calculator are estimates, not guaranteed outcomes.

You sit down to do your taxes and immediately feel overwhelmed. W2 forms, deductions, credits, tax brackets, standard versus itemized. And the big question looming over everything is, how much am I actually going to owe? Or better yet, am I getting a refund?

Most people wait until April to find out. They hand everything to a tax preparer or punch numbers into software and hope for good news. But here is the thing. You do not have to wait. You can estimate your tax bill right now, months before tax season even starts.

This is exactly why a US income tax calculator exists. It takes your income, deductions, and filing status, then shows you what you may owe in federal taxes or what refund you might get back. Running these numbers early helps you plan better, adjust your withholding if needed, and avoid surprises come tax time.

In this guide, you will understand how federal income tax calculators work, what a personal tax estimation tool shows you, how tax brackets actually function in the USA, the deductions and credits that lower your bill, and tax planning basics that help you keep more of your money. Let us get into it.

How Does a US Income Tax Calculator Work?

A US income tax calculator is a straightforward tool that estimates your federal tax liability. It asks for basic information about your income and situation, then calculates what you may owe based on current tax laws.

Here is what it typically needs:

- Your total income for the year, including wages, salaries, bonuses, and any other taxable income

- Your filing status, such as single, married filing jointly, married filing separately, or head of household

- Whether you take the standard deduction or itemize your deductions

- Any tax credits you qualify for, like the Child Tax Credit or Earned Income Tax Credit

- How much federal tax has already been withheld from your paychecks

Once you enter this information, the calculator shows you your estimated tax liability, what you have already paid through withholding, and whether you may owe more or get a refund. This gives you a clear picture of where you stand before you file.

Understanding How Federal Income Tax Brackets Work

One of the biggest misconceptions about taxes is how brackets work. Many people think that if you move into a higher tax bracket, all your income gets taxed at that higher rate. That is not true. The USA uses a progressive tax system.

Here is how it actually works. Your income gets divided into chunks, and each chunk gets taxed at a different rate. Only the income in a specific bracket gets taxed at that bracket's rate.

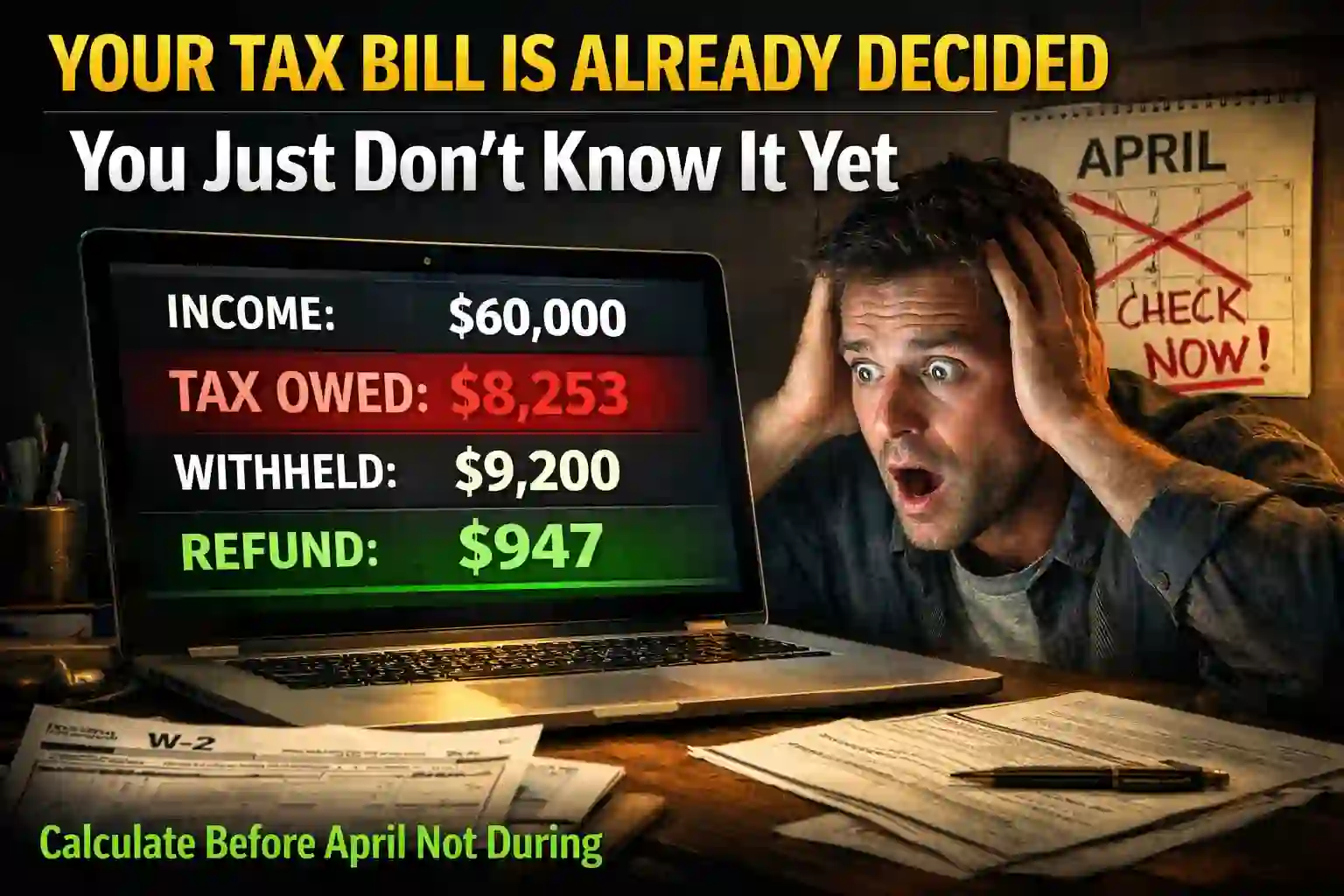

Let me show you an illustrative example using approximate 2026 tax brackets for a single filer. These figures are estimates to help demonstrate the concept. Always run your own numbers through a calculator for accurate projections based on your situation.

Say you earn $60,000 per year:

- The first $11,600 gets taxed at 10%, which is around $1,160

- Income from $11,600 to $47,150 gets taxed at 12%, which is around $4,266

- Income from $47,150 to $60,000 gets taxed at 22%, which is around $2,827

Your total federal tax is roughly $8,253. Even though you are in the 22% bracket, your effective tax rate is only around 13.8% because of how the progressive system works. A federal income tax calculator does all this math for you instantly.

Standard Deduction vs Itemizing: Which Saves You More?

One of the first decisions you make when filing taxes is whether to take the standard deduction or itemize your deductions. This choice can save or cost you thousands of dollars.

The Standard Deduction

For 2026, the standard deduction is estimated at around $14,600 for single filers and $29,200 for married couples filing jointly. You get this deduction automatically without proving anything. It reduces your taxable income dollar for dollar.

Most people take the standard deduction because it is simple and often gives them the biggest tax benefit. You claim it, your taxable income drops, and you are done.

Itemized Deductions

Itemizing means you add up specific expenses like mortgage interest, state and local taxes, charitable donations, and medical expenses. If your total itemized deductions exceed the standard deduction, itemizing saves you more money.

Common itemized deductions include:

- Mortgage interest on your home loan

- State and local taxes, capped at $10,000

- Charitable contributions to qualified organizations

- Medical expenses exceeding 7.5% of your income

A US income tax calculator lets you compare both options. You enter your deductions, and it shows you which method lowers your tax bill more. Many individuals use this feature to make sure they are taking the right path.

Tax Credits That Directly Reduce What You Owe

Here is something many people miss. Tax deductions reduce your taxable income. But tax credits reduce your actual tax bill dollar for dollar. That makes credits way more valuable.

For example, if you owe $5,000 in taxes and you have a $1,000 tax credit, your bill drops to $4,000. Simple math. No percentages. Just straight reduction.

Here are some common tax credits for 2026:

Child Tax Credit

You may get up to $2,000 per qualifying child under age 17. Part of this credit is refundable, meaning you can get money back even if you owe no tax.

Earned Income Tax Credit

This credit helps lower income workers and families. The amount varies based on your income and how many kids you have. It can be worth several thousand dollars and is fully refundable.

American Opportunity Tax Credit

If you are paying for college, you may qualify for up to $2,500 per eligible student. This helps offset tuition and education expenses.

Lifetime Learning Credit

This credit is for people taking college courses or job training. You can claim up to $2,000 per tax return for qualified education expenses.

A federal income tax calculator factors in these credits when you enter your information. It shows you how much each credit reduces your final tax bill, which helps you understand where your savings come from.

How Your Filing Status Affects Your Tax Bill

Your filing status is one of the biggest factors in how much tax you owe. The IRS uses different tax brackets and standard deductions for each status. Choosing the right one can save you thousands.

Single

You are unmarried or legally separated as of December 31. This status has the smallest standard deduction and enters higher tax brackets at lower income levels.

Married Filing Jointly

You and your spouse file one return together. This status typically offers the lowest tax rates and the highest standard deduction. Most married couples use this because it saves the most money.

Married Filing Separately

Each spouse files their own return. This rarely saves money, but some couples use it for legal or financial reasons, like keeping debts separate or dealing with complex situations.

Head of Household

You are unmarried and pay more than half the costs of keeping up a home for a qualifying person, like a child or parent. This status gives you better tax rates than filing single and a higher standard deduction.

When you use a US income tax calculator, entering the correct filing status is critical. The wrong status can inflate your tax bill by thousands of dollars or get you in trouble with the IRS.

Estimating Your Tax Refund or Amount Owed

The whole point of using a personal tax estimation tool is to see whether you are getting a refund or whether you owe money. Here is how that calculation works:

- The calculator figures out your total tax liability based on your income, deductions, and credits.

- It subtracts the federal income tax that has already been withheld from your paychecks throughout the year.

- If you paid more than you owe, you get the difference back as a refund.

- If you paid less than you owe, you have to pay the difference when you file.

Let me give you an illustrative scenario. Say your total tax liability is $8,500 for the year. Your employer withheld $9,200 from your paychecks. That means you may get a refund of around $700. But if your employer only withheld $7,800, you may owe around $700 when you file.

Running this calculation in advance gives you time to adjust your withholding if needed. Many individuals choose to tweak their W4 form mid year to avoid a big tax bill or to stop giving the IRS an interest free loan through overwithholding.

Common Mistakes People Make When Estimating Taxes

Even with a calculator, people still make mistakes that throw off their estimates. Here are the most common ones:

- Forgetting about income sources: They include their salary but forget about bonuses, freelance income, investment gains, or side gig earnings. All of that is taxable.

- Not accounting for tax credits: They enter their income and deductions but skip credits like the Child Tax Credit or education credits. This makes their estimate higher than reality.

- Using the wrong filing status: Filing as single when they qualify as head of household can cost them thousands in unnecessary taxes.

- Overlooking deductions: They take the standard deduction without checking if itemizing saves more. Or they miss deductions they qualify for, like student loan interest or retirement contributions.

- Ignoring state taxes: A federal income tax calculator only shows federal taxes. Many states also charge income tax on top of that, which can add another 3% to 10% or more to your total bill.

How to Use a Tax Calculator for Better Tax Planning

Here is where tax calculators become powerful. You do not just use them once at tax time. You use them throughout the year as a tax planning tool.

Here is how many individuals use calculators for tax planning basics:

- Run the calculator in January: Estimate your taxes early in the year based on your expected income. If you see you may owe money, you can adjust your withholding or set money aside.

- Update it mid year: Got a raise? Bonus? Freelance income? Run the calculator again to see how it affects your tax bill. You might need to increase your withholding.

- Test different scenarios: Thinking about contributing more to your 401k or IRA? Run the calculator with and without that contribution to see how much it lowers your taxes.

- Compare filing statuses: If you got married or divorced, run the calculator with both your old and new filing status to understand the tax impact.

- Check before year end: In November or December, run a final estimate. If you are going to owe a lot, you still have time to make extra estimated payments or increase withholding for the last few paychecks.

This proactive approach keeps you in control. No surprises. No scrambling at the last minute. Just smart tax planning basics that save you money and stress.

Understanding Withholding and How It Affects Your Refund

Your tax refund is not free money. It is your own money that you overpaid to the IRS throughout the year. And while getting a big refund feels good, it actually means you gave the government an interest free loan for 12 months.

Here is how withholding works. When you start a job, you fill out a W4 form. This form tells your employer how much federal tax to withhold from each paycheck. The more allowances you claim, the less they withhold. The fewer allowances, the more they withhold.

Many people aim for a small refund or a small amount owed. This means their withholding matches their actual tax liability pretty closely. They keep more money in their paycheck all year long instead of waiting for a lump sum refund in April.

A US income tax calculator helps you dial in the right withholding. You run your numbers, see what you may owe, and adjust your W4 if needed. Some employers even let you change your withholding online anytime.

When You Might Need to Make Estimated Tax Payments

If you are a W2 employee, your employer handles withholding for you. But if you have income that does not come with automatic withholding, you might need to make estimated tax payments four times a year.

This applies to:

- Self employed individuals and freelancers

- People with significant investment income

- Rental property owners

- Anyone with side income that does not have taxes withheld

The IRS expects you to pay taxes as you earn income, not just once a year. If you owe more than $1,000 when you file and you did not make estimated payments, you may face penalties and interest.

A federal income tax calculator helps you estimate how much to pay each quarter. You enter your expected income, and it shows you what your quarterly payment should be. Many individuals set reminders to run the calculator and pay on time in April, June, September and January.

For more details on estimated tax payments, the IRS page on estimated taxes provides official guidance and payment deadlines.

How Tax Law Changes Affect Your Calculations

Tax laws change almost every year. Congress adjusts tax brackets for inflation, modifies deduction amounts, creates new credits, or phases out old ones. This means your tax situation can shift even if your income stays the same.

For example, the standard deduction goes up most years to keep pace with inflation. Tax brackets also adjust, which means you might stay in the same bracket even if you get a small raise. These changes are usually announced late in the year before they take effect.

This is why you need to use a calculator that stays current with tax law. An outdated calculator using 2024 numbers will give you wrong estimates for 2026. Many individuals choose calculators that update automatically or check for updates before running their numbers.

Final Thoughts: Know Your Numbers Before Tax Season Hits

Look, taxes are stressful enough without walking in blind. You do not need to wait until April to find out if you owe money or get a refund. You can run the numbers right now and know exactly where you stand.

Take 10 minutes today. Gather your income information, enter it into a US income tax calculator, and see what your tax bill looks like. If you are getting a huge refund, maybe adjust your withholding so you get more money in your paycheck all year. If you are going to owe, start setting money aside now.

The key is control. When you know your numbers, you make better decisions. You plan ahead. You avoid surprises. And you keep more of your hard earned money where it belongs, in your pocket.

You can calculate your estimated federal income tax and explore different scenarios using the DollarMento Tax Calculator. It takes just a few minutes and gives you a clear picture of your tax situation for the year.

Frequently Asked Questions

Q1. How accurate are income tax calculators?

Income tax calculators provide estimates based on the information you enter. They use current tax laws and brackets to calculate your liability. The accuracy depends on how complete and accurate your inputs are. If you include all your income, deductions, and credits correctly, the estimate will be close to your actual tax bill. However, complex tax situations may require professional help for precise calculations.

Q2. What is the difference between marginal and effective tax rates?

Your marginal tax rate is the rate you pay on your last dollar of income, which is your tax bracket. Your effective tax rate is your total tax divided by your total income, which is usually much lower. For example, you might be in the 22% bracket but have an effective rate of 14% because lower portions of your income get taxed at lower rates. A US income tax calculator typically shows both rates.

Q3. Should I itemize deductions or take the standard deduction?

Take whichever saves you more money. For 2026, the standard deduction is estimated at around $14,600 for single filers and $29,200 for married couples filing jointly. If your itemized deductions like mortgage interest, state taxes, and charitable donations total more than the standard deduction, itemize. Otherwise, take the standard. A calculator can compare both for you.

Q4. How do tax credits differ from tax deductions?

Tax deductions reduce your taxable income. Tax credits reduce your actual tax bill dollar for dollar. Credits are more valuable. For example, a $1,000 deduction might save you $220 in taxes if you are in the 22% bracket. But a $1,000 credit saves you $1,000 in taxes regardless of your bracket. Always claim every credit you qualify for.

Q5. What filing status should I use?

Your filing status depends on your marital and family situation as of December 31. Single if unmarried, married filing jointly if married and filing together, married filing separately if married but filing alone, head of household if unmarried and supporting a dependent. Most married couples save the most by filing jointly, but a calculator can show you both options to confirm.

Q6. Why is my tax refund different from what the calculator showed?

Several reasons can cause this. You might have forgotten to include income sources when using the calculator. Your withholding amount might have been different than you entered. Tax laws might have changed between when you ran the calculator and when you filed. Or you might have claimed different deductions or credits on your actual return. Always use the most current calculator with complete information.

Q7. Do I need to pay estimated taxes if I have a side job?

If you earn income that does not have taxes withheld, like freelance work or side gig income, you may need to make quarterly estimated tax payments. The IRS expects you to pay taxes as you earn income. If you expect to owe more than $1,000 when you file, many individuals consider making estimated payments to avoid penalties. A federal income tax calculator can help you estimate what to pay each quarter.